Notes On The Allegory Of The Hawk and the Serpent

Published by Artemis Capital, the paper looks at allocating assets for 100 years

“Imagine you have the opportunity to grant your family great wealth and prosperity for 100 years; but you must decide what assets to invest in and maintain that allocation for an entire century without ever changing it. The future of your children’s children depends on your decision. What do you do?”

This is Artemis Capital Management’s outstanding piece, The Allegory of the Hawk and the Serpent, How to Grow and Protect Wealth for 100 Years.

Chris Cole and his team put a lot of thought and effort into this research. Highly recommend reading the entire piece, absolutely outstanding, and has heavily influenced how I think about diversification, concentration, and long term wealth building.

I originally took these notes eight months ago. Where I have updated thoughts, they will be in italics.

Great starting point to understand the framework of this paper is watching Chris’s interview with Danielle DiMartino Booth for RealVision, which is now free on youtube before diving into the full report.

Please keep in mind I am an individual investor with a day job, these are just my personal notes on Artemis’s paper, none of it is advice.

Artemis’s research tests modern portfolio strategies through four generational seasons (20 years) and one lifetime (90 years) going back to 1928 to learn about potential futures.

I like taking a long view, and have personally had history affect my future overseas, so the approach makes sense to me.

What Artemis found testing modern portfolio strategies is while they performed well during times of secular growth (symbolized by the Serpent) they did not do well during times of secular change (symbolized by the Hawk).

Updated Note 1/04/2021: For clarity, think of secular growth as the business cycle, increasing GDP and relative stable/low volatility as assets like equities, real estate, and bonds all do well. For secular change, that can come in two versions, either inflation or deflation which will be accompanied by higher volatility which will have liquidity and solvency challenges for traditional secular growth assets.

Assets that are geared for secular change will do well, like long volatility, commodity trend following, gold, and cash depending on whether a right or left tail secular change, with one and then the other also being possible.

I now think of this paper as showcasing the power of being balanced, being efficient in asset allocation to grow wealth but also durable, so I do not have to guess what the future holds, but will be able to thrive since instead of guessing about an outcome I have no control and little insight on am focused on maintaining balance in my own wealth and asset allocation to thrive as the future unfolds into reality.

Being balanced allows for a mental nimbleness and clarity which emotion and stress will cloud and obfuscate, “the fog of war” when you most need clarity to win is now how I think of this now.

End updated note

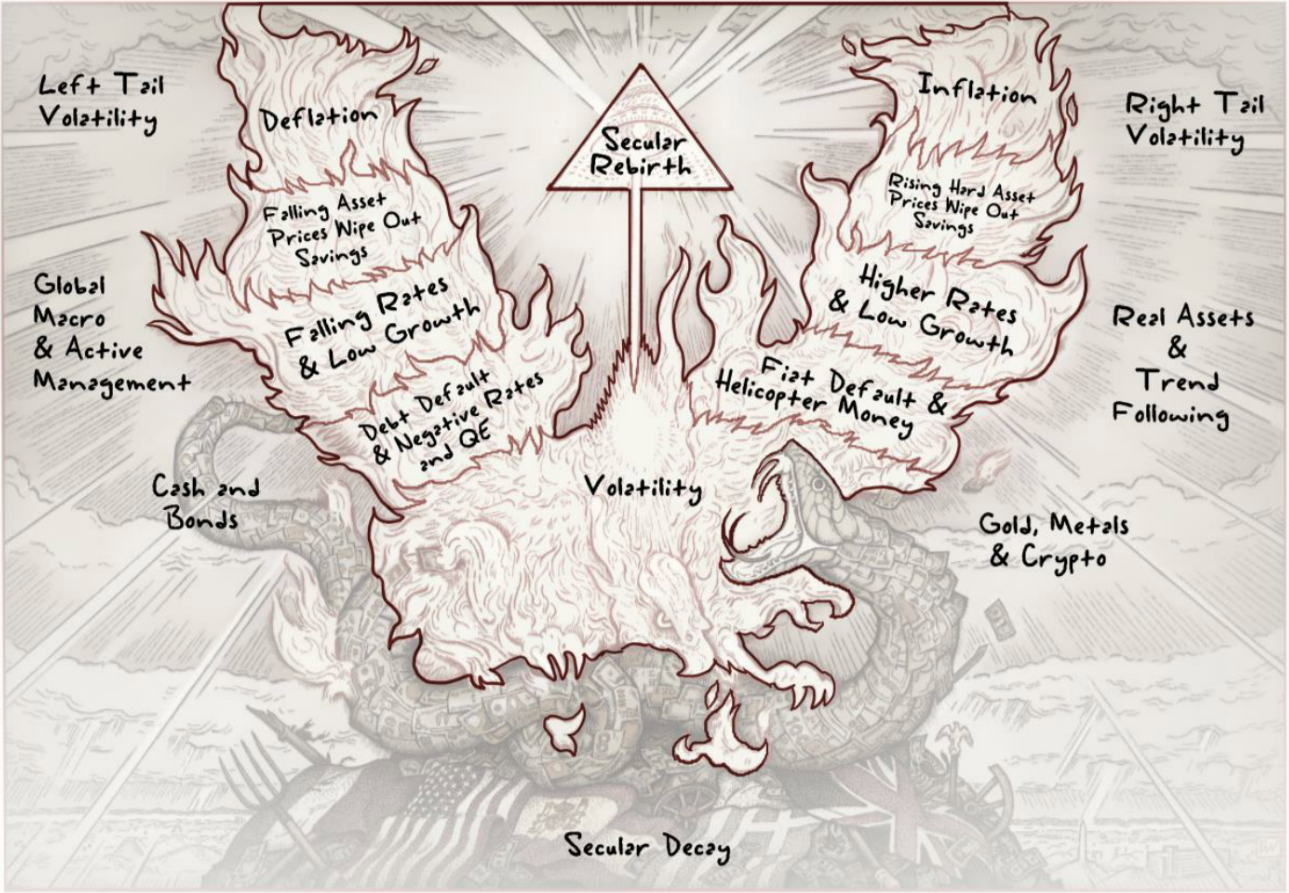

The allegory of the Hawk and the Serpent helps orientate an investor on making choices that protect wealth from the threats posed by the secular change of either deflation or inflation (The Hawk) while steadily compounding wealth during times of secular growth (The Serpent).

“The greatest threat to 100 years of prosperity is neglecting the lessons from long-term financial history and having no true diversification against secular change.”

Artemis - “To make our fortune we must first understand our place in history.”

For the first time since the 1930’s, we’re seeing secular change challenge the secular growth which US has enjoyed.

We’re at the end of a 40 year demographic and debt super-cycle that started when Baby Boomers joined the work force and has now run its course as they retire.

Modern portfolio strategies have performed admirably. But what happens when you look back further than 1980?

If you would have bought on market declines consistently between 1929 and 1970 you would have gone bankrupt three times.

Passive indexation would have realized -86% peak to trough decline in 1930’s and two decades of lost performance.

91% of the price appreciation for a traditional 60% stocks, 40% bonds portfolio comes from just the last 22 years (1984-2007) out of the last 90 years.

72% of the performance in home values were from this period as well.

Basically the mantra “buy on weakness” and passive indexation would not have worked for most of the last 90 years.

So why do traditional strategies perform poorly over the longer time frame of 90 years?

The mean reversion and low volatility people assume is normal today isn’t forever.

In secular declines like the 1930s, or stagflationary recession like late-1960s to 1970s there is a perpetual trend lower in asset prices and trend higher in volatility that persists for years.

That is an incredibly bad environment for all the sophisticated investors who are leveraged up and selling volatility counting on lower volatility with higher asset prices.

“The average institutional and retail portfolio is essentially a wager that the once in a lifetime returns from the secular boom of 1984-2007 will somehow repeat, against all historical odds.”

So if modern portfolio theory has limitations over the long timeframe in dealing with secular change, then what is another answer?

Cosmic duality, or the middle path. Never being black or white, but balanced.

Personally, I happen to agree with Artemis on this and not just for investing, but for life in general.

Updated Note 01/05/2021: I have really been thinking hard about a balanced portfolio over most of the last year, with a global pandemic, US election, riots in cities, Fed response, if a person was constantly trying to decide what to do in markets it would be exhausting. Honestly think zooming out, trying to stay balanced on the portfolio is how I want to ensure my own long term success, but have noticed it is not easy, takes an almost emotional toll and self-discipline to do it, which is likely why most don’t. It is hard to take responsibility for your own portfolio construction, looking at investments as pieces of a larger holistic portfolio and takes what used to be exciting (market news, Fed response, studying macro trends) and largely makes it almost boring. It was disconcerting at first, realizing to be balanced it was ok not to have an opinion on everything, and then realizing really there wasn’t much that made a difference, and I was better off focusing on making money and allocating that capital correctly. That is when the genius of the balance and the long view of this approach really became evident.

End update note.

I have had a lot of success on different continents implementing a middle path strategy at work.

Starting out it can be tough to conceptualize the long view and understand why giving up the immediate tactical win for the strategic victory further off is important, but as the years pass, and you see results, it becomes easier.

Artemis mentions the hard part with this isn’t investing, but social since most around you won’t understand what you are doing.

I would agree with this, too. Once had a baby boomer supervisor who treated helo pilots like his personal Uber service fly out to tell me I was going native.

The middle path is definitely not for those who are unsure of themselves.

Artemis uses a simple example to illustrate the point of the middle path in investments below in three assets.

Assets A and B closely track each other and the business cycle in a positive trend. Asset C countertrends and makes less profits opposite the business cycle.

Which two would be best to combine?

“Those who place the power of man above the natural laws of the universe do so at their peril. If you only focus on investing for the growth cycle, thinking that growth will continue unabated forever ignores the lessons from thousands of years of human civilization.”

Long term success depends on embracing the inevitability of growth being disrupted and seeking balance to preserve and grow wealth through whatever happens in the future.

100% agree. Think modern portfolio theory has over-optimized efficiency at the sake of durability which is always a mistake, whether investing or life.

Enter the Dragon

Combining the holdings of secular growth (the Serpent) with holdings that perform well on the wings of secular change, either deflation or inflation (the Hawk) you get a portfolio that is the middle path of cosmic duality, The Dragon.

“The solution to the successful 100-year portfolio is unbelievably simple when you study financial history: find assets that can perform when stocks and bonds collapse, and boldly own them regardless of short term performance…To thrive over 100 years, balance assets that profit from secular growth with those that profit from secular decline.”

Long volatility, gold, commodity trend, and discretionary global macro should be core portfolio holdings, much like bonds, not just token positions in the portfolio.

Artemis learned from their in-depth study (over 20 pages of quantitative notes on each asset class and timeframe in the report) of financial history that investors should prioritize secular non-correlation over excess returns.

The optimal portfolio since 1929 is vastly different than the median US portfolio made up of mostly stocks, then bonds, with a bit of cash:

Domestic equities (24%)

Fixed Income (18%)

Active Long Volatility (21%)

Trend Following Commodities (18%)

Physical Gold (19%)

The Dragon portfolio substantially outperformed all alternatives throughout the last 90 years when adjusted for risk across all economic environments compounding at 14.4% per year and 15% annualized volatility between 1928 and 2019.

Assets which do well in growth phases are equity, credit, and real estate.

Assets which do well on the left wing of the hawk in deflation are global macro and active long volatility while assets that do well on the right wing of inflation are real assets, gold, and commodity trend following.

Combining all assets in a balanced portfolio leads to returns in all environments.

Artemis says active long volatility is one of the most under-allocated assets. Primary value add of active long vol is anti-correlation to the growth cycle and explosive performance during market crisis.

Discretionary global macro investing has traditionally served as a defensive style of investment but there is no way to test this asset class systemically into the past so it has been excluded, but Artemis urges its consideration.

On the subject of fixed income/debt, for real estate, someone who has put 20% down on a mortgage has replicated 5x leverage exposure to the business cycle.

Real estate had the highest return adjusted to risk of any single asset Artemis tested over 90 years.

For the 10-year treasury bond to repeat gains from 2008, yield would have to fall to -1.5%.

I have a hard time visualizing the 10-YR at -1.5%, but don’t think it is impossible. Some people have a near violent reaction when you suggest the possibility. Agree it would have social implications if it happens. We’ll see what the future holds.

On gold, agree with Artemis, I like buying and holding physical gold…always looked at it as more insurance than investment but my view is changing.

Updated Note 01/05/2021: Have been thinking more about gold, and instead of holding it physically, have been looking at the benefits of offshore storage, so not only is it working as an investment in the portfolio, but it is also hedges me against geopolitical risk by having asset physically stored in a different hemisphere, if I do this, will write an article on the details in the Fortress.

End note.

To end where we started, at the original question, if I had to make one choice for the next 100-years, what is the simple answer?

Build a Dragon portfolio with passive investments that track S&P500 (Equity), Bloomberg Barclays US Treasury Bond Total Return Index (Bonds), own physical Gold, and a portfolio of hedge funds from the HFRX Macro Systematic Diversified CTA Index (Commodity Trend) and Eurekahedge CBOE Long Volatility Hedge Fund Index (Active Volatility).

Done. See you in 2120. Well, I won’t, but the money will.

My thoughts on adapting the strategy as an Individual Investor

Now, lets talk about how I am looking at adapting this as an individual investor, which in some ways is a distinct advantage.

It can’t be easy trying to convince voting family members on a $150 million family office that what has worked well for the last 40 years may not work so well in the future, so lets build a dragon portfolio.

Of course the disadvantage is obvious as well, not being to the point of allocating to a portfolio of hedge funds to protect against the tail risks of deflation and inflation, so just have to improvise.

What that looks like for me, I think, is something like this.

I had to think about this for a couple weeks after I first read the research. I need to stress I’m not selling any assets and reallocating. Why pay the capital gains taxes when I can just shift current income and grow the underrepresented allocations slowly with total net worth and income increases over time?

Lets start with the growth part of the portfolio - Equities and Bonds/Real Estate.

I’m not making any changes to my current equities portfolio. I don’t own much in bonds to speak of, have some $TLT, but I really look at my federal pension I’ll qualify for so long as I don’t get blown up (again) or die in a car wreck somewhere in a desert hours from a hospital (more common than you would think) in another ten years as my bond investment.

I’ll get paid dollars each month, which is pretty much what treasury bonds do, so for right now, I’m using that as a stand in for that part of the allocation.

Eventually would like to have real estate eclipse that and take over that part of the percentage pie, since it was the top risk-adjusted return in last 90 years. That just probably won’t happen while working overseas and living like a gypsy.

Updated Note 01/05/2021: Have been thinking hard on real estate and studying, and thinking what I would like to eventually do is be a limited partner in private real estate funds so I can have exposure in real estate while working around the world. This will take a few years to implement as minimum investments range from $100k-$250k.

End note.

For the left tail volatility of the Hawk, deflation, I will be upgrading to Real Vision Pro and use the trading portfolio that has input from Raoul Pal and Julian Brigden to start trading Global Macro.

Updated Note 01/05/2021: While I still will be upgrading to Pro for the trading portfolio and because I genuinely enjoy keeping up with global macro, think I would prefer to make an investment as an LP in a long volatility fund as the primary instrument. When I do so, will write an update in the Fortress.

End note.

On the right tail of volatility, inflation, I was already considering taking the gold up from 5% to 10%, and honestly I have no problem taking it up to 19% of the portfolio.

Now lets talk about Bitcoin, which is on the right side against inflation as well.

I look at this portfolio as one I will be growing into. Currently I am very heavy into bitcoin, but over time will be rebalancing in as tax efficient manner as I can to get to a more balanced portfolio.

So to recap, big changes coming out of this for me will be adding global macro trading and maybe starting to save for real estate in the future.

See you out there. - RC